What is the Tax Amortisation Benefit (TAB)?

Tax amortisation benefit (TAB) refers to the net present value of income tax savings resulting from the amortisation of intangible assets. Amortisation of assets decreases the net taxable income and thereby the corporate income tax to be paid as cash.

When the purchaser of an intangible asset is allowed to amortise the price of the asset as an expense for tax purposes, the value of the asset is enhanced by the present value of the future tax savings allowed by the amortisation. This idea is analogous to the treatment commonly afforded to depreciation expense in net present value calculations.

How does the TAB affect the fair value of an intangible asset?

The TAB is added to the value of the intangible asset on the premise that a potential purchaser will be willing to pay an amount that reflects the present value of the tax amortisation benefit.

What do IFRS and US GAAP say about including tax amortisation benefits in the fair value of intangible assets?

One should always recognize the value of amortisation benefits when the purpose of the appraisal is a purchase price allocation for financial reporting purposes according to IFRS and US GAAP. The inclusion of tax amortisation benefits in fair value is implicit in FASB Accounting Standards Codification 740 Income Taxes (ASC 740), which requires assets acquired and liabilities assumed to be stated at their “gross” fair value, even if the transaction happens to be a non-taxable business combination rather than an asset purchase.

Should the TAB factor be applied to the value of intangible assets under every valuation method?

No. It is correct to apply the TAB factor if the intangible asset is being valued through an income approach valuation (i.e. DCF, Relief from Royalty). However it is incorrect to apply the TAB factor if using a market approach (i.e. multiple valuation). In the market approach, value is estimated from market prices paid for comparable assets and the prices shall contain all benefits of owning the assets (including tax amortisation benefit).

Should the TAB factor be applied to the value of intangible assets in all countries?

No. Some countries do not allow tax amortisation of some types of intangible assets. In such cases, the TAB factor will equal 1.0 (no tax amortisation benefit). Check these countries in our detailed table.

Asset deal vs. share deal: Realization of TAB and recognition of a deferred tax liability (DTA)

In an asset deal, the acquirer will activate the acquired intangible asset at its fair value. Thus, the acquirer will be able to realise TAB on the excess of the fair value of an asset over its previous book value (“Hidden Reserves”).

In a share deal, hidden reserves are only recorded as accounting consolidation adjustments on the acquirer’s financial statements and the tax bases of the assets are not adjusted. Consequently, in a share deal a deferred tax liability needs to be booked in the acquirer's consolidated financial statements.

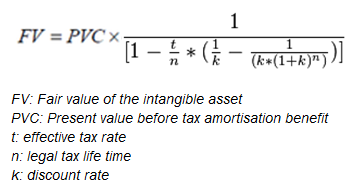

The present value of the tax savings caused by the amortisation of an asset is a mathematical function of its fair value. This creates circularity, because the fair value should include the present value of the tax savings. To escape from this circle valuators can either perform an iterative calculation, or calculate the TAB separately by applying a step-up factor to the value of the asset before amortisation benefits. In the latter approach, the value of the intangible asset is estimated in the absence of the tax amortisation benefit first and is then grossed up by a tax amortisation benefit factor, leading to the fair value of the asset.

Considering the tax amortisation lifetime allowed by country-specific tax legislation and assuming that the amortisation schedule is straight-line and that tax rules allow amortisation of the full Fair Value of the asset, the present value of tax savings due to amortisation becomes a straightforward mathematical calculation once having determined the appropriate discount rate.

The TAB is calculated by using a two-step procedure:

Step 1: Value the asset in the absence of amortisation benefits. This is accomplished by calculating the discounted present value of the after tax cash flows attributable to the asset, where the cash flows do not reflect amortisation charges in the tax calculation. Examples of methods commonly used in Step 1 are the Relief from Royalty Approach, the Excess Operating Profit Approach and the Cost Savings Approach (not to be confused with the "Cost to Replace" Approach).

Step 2: Incorporate the present value of tax savings due to amortisation by "grossing up" the value from Step 1 by a TAB Factor. The calculation of the TAB factor is performed by the Online TAB Calculator of this site.